From the Seiberlich Accountancy Corporation

In September 2013, the IRS and U.S. Treasury issued final capitalization regulations. These revised regulations, under specified circumstances, permit business taxpayers to make safe harbor elections that would enable them to deduct expenditures that might otherwise need to be capitalized. The focus of this alert is on the de minimis safe harbor election and the requirement for taxpayers to have a written accounting policy in place not later than the first day of their tax year — January 1, 2014 for calendar year clients.

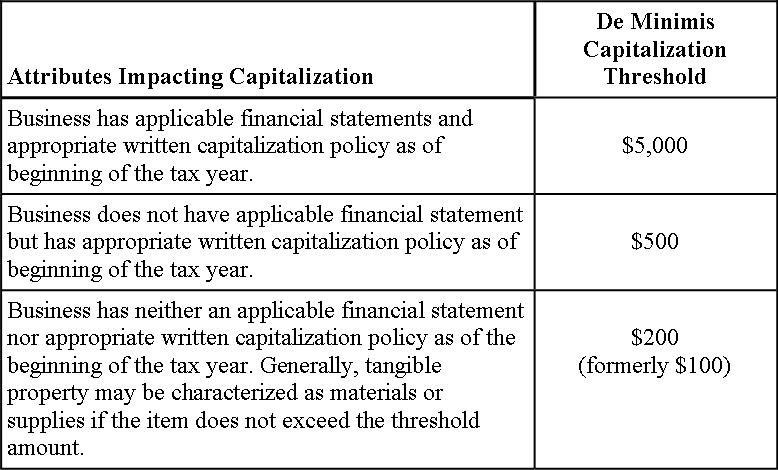

What amount is considered de minimis?

The amount considered de minimis under the de minimis safe harbor election depends upon whether the taxpayer has written accounting procedures (“accounting policies”) in place and, if so, whether the taxpayer has an applicable financial statement. As long as business taxpayers have written accounting policies in place at the beginning of the tax year, the de minimis amount may be as high as $5,000 for those with an applicable financial statement and as high as $500 for those without an applicable financial statement. Those taxpayers without written accounting policies in place will still be permitted to characterize tangible property as materials or supplies for items costing $200 or less.

What is an applicable financial statement?

The applicable financial statement is a taxpayer’s financial statement with the highest priority. The list below details the financial statements in the order of priority, with the highest priority appearing first:

(1) Financial statement required to be filed with the SEC

(2) Audited financial statements used for credit purposes

(3) Audited financial statements used to report to shareholders, partners or similar persons

(4) Audited financial statements used for another substantial non-tax purpose

(5) A financial statement (not a tax return) required to be provided to the federal or state government or any federal or state agency

Note: Presumably, reviewed, compiled and taxpayer-prepared financial statements not reported on by CPAs would only be considered applicable financial statements if required to be provided to government entities.

How are de minimis safe harbor elections to be made?

The election is made by attaching a statement to a timely filed original Federal tax returns (including extensions) for tax years in which the additional deductions are sought. The statement must be titled “Section 1.263(a)-1(f) de minimis safe harbor election” and include the taxpayer’s name, address, taxpayer identification number, and a statement that the taxpayer is making the de minimis safe harbor election under Treas. Reg. § 1.263(a)-1(f).

When are the final regulations effective?

The new regulations are effective for years beginning after December 31, 2013.

May the election be made for prior year returns?

Yes, taxpayers may choose to apply Treas. Reg. § 1.263(a)-1(f) to tax years beginning before January 1, 2014 and after December 31, 2011. The election would need to be made on an amended return for the applicable year on or before 180 days from the due date, including extensions, of the taxpayer’s tax return for the applicable tax year. The final regulations may be applied retroactively, but many taxpayers will only be able to use the safe harbor in future tax filings because the de minimis safe harbor provision requires written accounting policies in place on the first day of the applicable tax year.

Can the temporary regulations still be used?

The temporary regulations may no longer be used for tax years beginning after December 31, 2013. However, they may still be used for tax years beginning before January 1, 2014 and after December 31, 2011. Unlike the final regulations, the temporary regulations’ de minimis safe harbor provision contains an aggregate ceiling. Thus, where the option to apply the temporary regulations and the final regulations are available, consideration should be given to the limitations and benefits of each.

Other applicable rules could complicate the issue and minimize the benefits available.

What does this mean?

Businesses that wish to make the de minimis safe harbor election will need to have written accounting policies in place by the beginning of their tax year (1/1/2014 for calendar year taxpayers) and make the election on a timely filed original return.

Where can I go for additional guidance?

For specific instructions:

• Internal Revenue Bulletin 2013-43 (T.D. 9636) at http://www.irs.gov/irb/2013-43_IRB/ar05.html contains final regulations that provide guidance on the application of IRC §§ 162(a) and 263(a) to amounts paid to acquire, produce or improve tangible property (i.e., final capitalization regulations);

• Treas. Reg. § 1.162-3 provides for the treatment of materials and supplies;

• Treas. Reg. § 1.162-4 provides for the treatment of repairs and maintenance;

• Treas. Reg. § 1.263(a)-1) provides for the treatment of capital expenditures;

• Treas. Reg. § 1.263(a)-2 provides for the treatment of amounts paid for the acquisition or production of tangible property; and

• Treas. Reg. § 1.263(a)-3 provides for the treatment of amounts paid for the improvement of tangible property

If you think these changes may affect you, give us a call if you have any questions regarding these changes. If you would like to receive a Sample Capitalization Policy, please call us at (925) 939-8222 or email to Jeannie@seibercpa.com.

60 Mayhew Way. Walnut Creek, CA 94597-2091

Phone: 9925) 939-8222. Fax (925) 939-0112. Toll Free: 800.6100. CPA.

Email: info@SeiberCPA.com

***